Sites

Authors: Ryan Kastner

Two frogs lived together in a marsh. But one hot summer the marsh dried up, and they left it to look for another place to live - for frogs like damp places if they can get them. By and by they came to a deep well, and one of them looked down into it and said to the other, “This looks like a nice cool place. Let us jump in and settle here.” But the other, who had a wiser head on his shoulders, replied, “Not so fast, my friend. Supposing this well dried up like the marsh, how should we get out again?” – Aesop’s fable “The Two Frogs and the Well”

In today’s modern economy, asset managers are well-equipped to protect a pension plan’s financial position from many risks. Interest rate hedging, long duration fixed income, inflation swaps and increased allocation to alternative asset classes stand strong against even the most challenging economic environments.

With powerful analytical tools and sophisticated modeling techniques keeping market risk under control, longevity risk, the loss that a pension plan might face should its members live longer than expected, stands as the next great threat. Despite all the advances in market risk mitigation strategies, little exists, and even less is done, for longevity risk management from an investment standpoint. Even the most thorough actuarial analysis has proven unable to consistently predict Canadian human mortality with any level of precision.

In addition, every revision to the best-estimate mortality assumption for Canadian pensioners to reflect longer life expectancies comes with increased pension liabilities and a deterioration of a plan’s financial status. However, unlike investment assumptions which are reviewed on a regular basis, an outdated mortality table may remain in use for many years and only be updated following the release of a new study.

This being the case, asset managers can easily become overly focused on current issues, overlooking past experiences and remaining willfully blind to impending longevity risks. In essence, when it comes to longevity, we have acted like the foolish frog from Aesop’s fable.

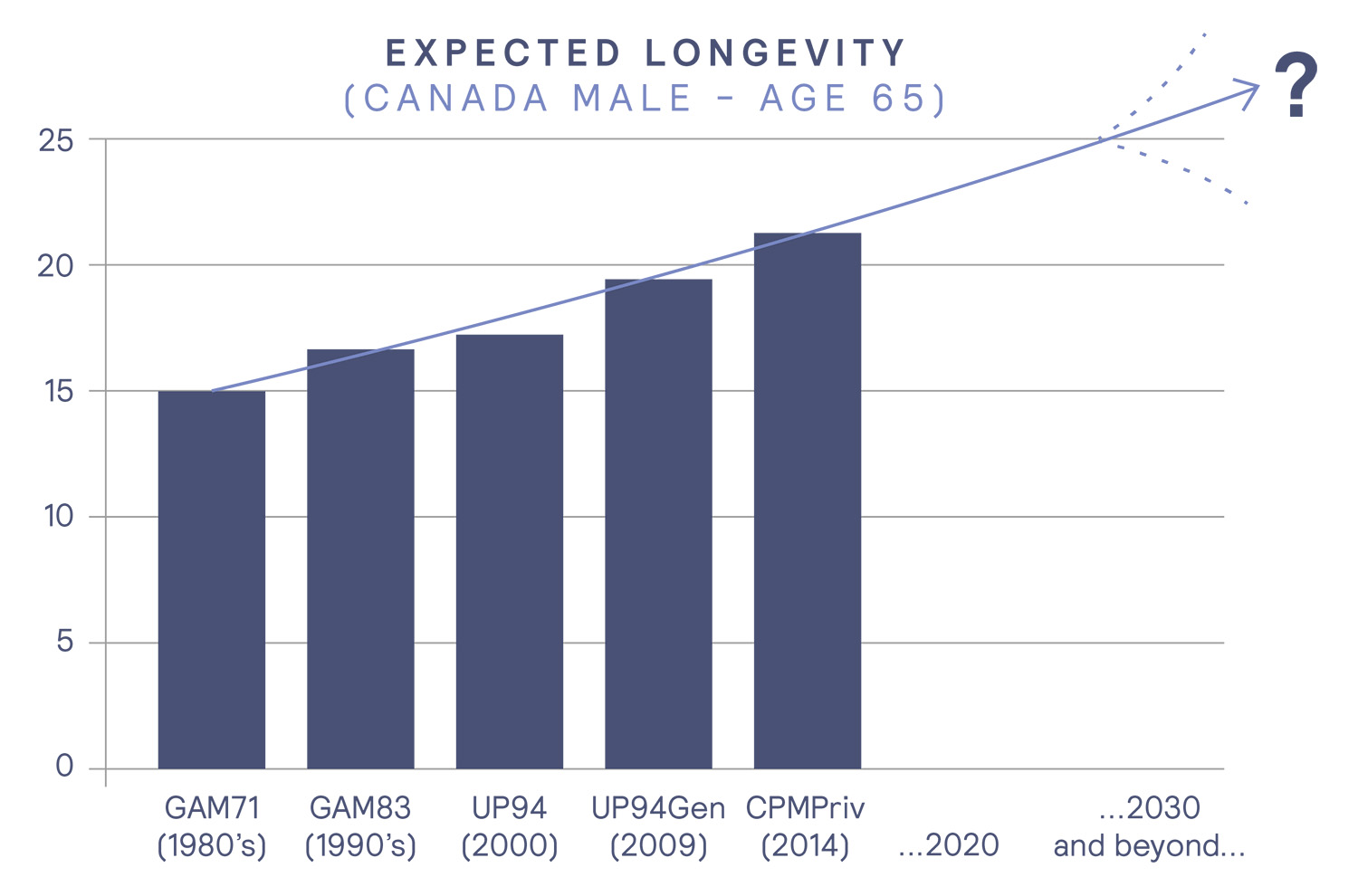

In the late 1970s and 1980s, the life expectancy for a 65-year-old male pensioner was just over 70 years old. Since then, actuaries’ best-estimate assumptions have been revised several times. The most recent study released by the Canadian Institute of Actuaries indicated that the life expectancy of a 65-year-old male had increased to 87 years (Figure 1). As pensioners live longer than initially predicted, these previously understated longevity expectations, which may not have been reflected in initial liability estimates for pension plan valuations, risk emerging later as valuation losses. Depending on the characteristics of the plan, the pension obligation may increase up to 8% for every one-year increase in life expectancy. Looking back over the past 40 years, pension plan liabilities have increased significantly due solely to longevity.

Purchasing annuities has become a more popular solution to protect a pension plan from longevity risk. This strategy, however, leads to other complications such as up-front payment of premium and, in many cases, immediate recognition of a loss in the plan’s financial statements.

In addition, an annuity purchase transfers the market risk and administration responsibility of the pension payments which, for human resources, public relations or cost considerations may not be desirable.

One alternative to consider which has become quite common in the United Kingdom is a longevity swap. The first pension longevity swap was executed in 2008. Since then, that market has totaled over $100 billion CAD, half of that amount being related to transactions which occurred in 2014 (Figure 2).

![]()

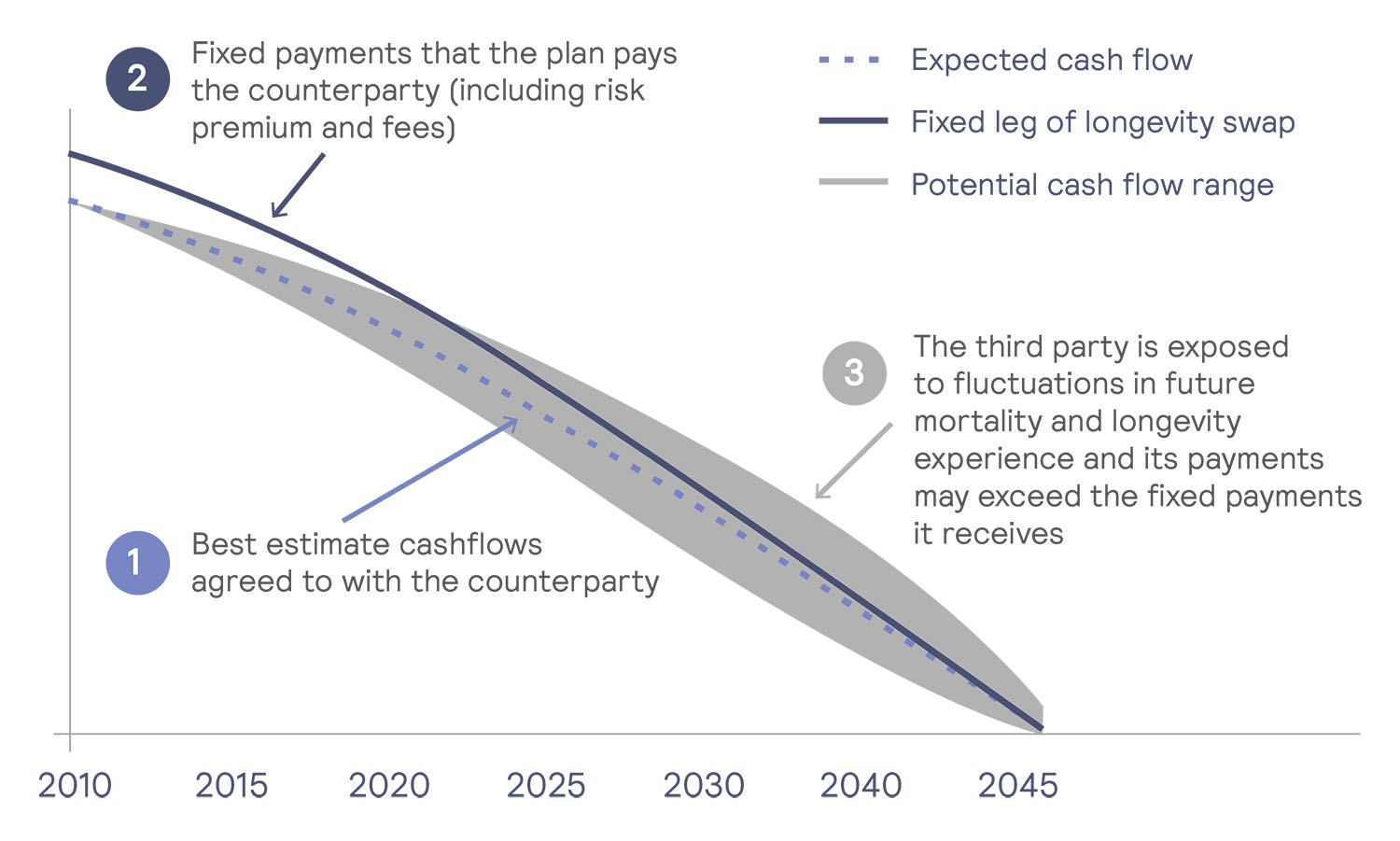

As illustrated in Figure 3, a longevity transaction entails an exchange of cash flows with a counterparty whereby, for a premium, the insured pension plan trades its obligation to pay its pensioners according to their actual lifespans (known as the floating leg) for a fixed payment schedule (often referred to as the fixed leg).

Such a transaction is seamless for retirees; the pension plan continues to pay its pensioners, but the difference between the fixed and floating legs is netted out and settled on a monthly basis between the two counterparties to the transaction.

A typical longevity swap can cover a significantly large liability, usually with a face value in the billions of dollars, as the protection is only applied to deviations versus initial expectations. Given the size of these transactions, it is not uncommon for the front insurer to seek reinsurance agreements. In most swaps, the front insurer will cover less than 20% of the deal.

The fixed leg of the swap is constructed as the combination of three distinct items:

As opposed to an annuity purchase where the premium is paid up-front, in a longevity swap the premium is paid monthly as part of the fixed leg and risk exposure is symmetrical (either party might be obligated to pay depending on the actual longevity of covered pensioners). However, payment of what is owed to the party “in-the-money” will only be paid over time as expectations are, or are not, realized. This deferred nature of the settlement payments introduces counterparty risk to the side that believes that future experience will be in its favour. This issue can be of particular concern in cases where there is a strong indication that the current best-estimate assumption is incorrect but experience has yet to emerge as may be the case, for example, following the spread of a deadly disease or discovery of a cure for cancer.

Consequently, longevity swaps usually contain some form of protection against the other party’s inability or unwillingness to pay. In the United Kingdom, where the longevity swap is more common, traditional practice has been to establish collateral accounts for both the fees payable by the insured to the insurer and the experience amount that is expected to be paid in the future. These accounts tend to be valued daily with every dollar of risk exposure collateralized. However, other credit risk mitigation techniques can also be used.

Alternative strategies have included “resetting” the fixed leg with a cash payment to reflect the revised mortality assumption once experience begins to stray too far from expected or using a collateral account approach but with significantly high thresholds to limit the frequency of having to post collateral.

Ultimately, the structure of the counterparty credit risk mitigation and the extent to which it serves as protection should not be predetermined but rather negotiated among all parties and customized on a deal-by-deal basis.

Although the mechanics of the process remain the same, a longevity swap can be structured as either an insurance product or as a bank derivative. A swap classified as an insurance product will generally fall under insurance legislation and be subject to their capital requirements. This might be particularly onerous when trying to include a foreign reinsurer, as they too will be subject to these regulations. A longevity swap that is designed to be a derivative product will be governed by an ISDA (International Swap and Derivative Association) agreement signed between the two parties.

Recently, longevity swaps have started gaining traction in Canada. In March 2015, Bell Canada announced that it had entered into a longevity swap with Sun Life. This was the first transaction of its kind completed outside of the UK. With an underlying face value of $5 billion CAD, it was the largest de-risking transaction ever done in Canada and the 5th largest globally.

Looking at pension plans going forward, care must be taken not to disregard the potential loss due to adverse longevity experience. That’s not to say that every plan must act to hedge this risk – different plans have different risk profiles and different plan sponsors have different risk appetites. However, we must acknowledge that this exposure exists and plan accordingly. We must act like the wise frog from Aesop’s fable and learn from our past mistakes. We must think before we leap.

RYAN KASTNER, FSA, FCIA, FRM

MERCER FINANCIAL STRATEGY GROUP

Ryan is a member of Mercer’s Canadian Financial Strategy Group. Over the course of his career, Ryan has been involved in many projects in the innovation and de-risking space. He played an integral role in the development of the Mercer Pension Risk Exchange, a global online platform for group annuity purchases, as well as the $5 billion longevity swap between Bell Canada and Sun Life, the first pension longevity insurance arrangement transacted outside of the United Kingdom.

Ryan holds a Bachelor of Science degree from McGill University where he majored in Mathematics and Statistics. He is a Fellow of both the Society of Actuaries and Canadian Institute of Actuaries.

BENOIT HUDON, FSA, FCIA

PARTNER, MERCER (CANADA) LIMITED

MERCER RETIREMENT INNOVATION LEADER, CANADA

Benoit Hudon manages Mercer’s Retirement business in Eastern Canada. He is also Mercer Canada’s Retirement Innovation Leader. He has been providing risk management consulting services for close to 20 years.

Benoit has extensive experience consulting to national and international clients on retirement issues. Throughout his career, Benoit has contributed extensively to the development of pension risk management models and consulting solutions. He has developed sophisticated and holistic solutions for organizations in the manufacturing and financial sectors. More recently Benoit acted as lead advisor on the first pension longevity insurance transaction concluded outside of the United Kingdom, a $5 billion longevity swap between Bell Canada and Sun Life.

Benoit holds a Bachelor’s degree in Actuarial Sciences from Université Laval and is a Fellow of both the Society of Actuaries and the Canadian Institute of Actuaries.

By clicking Submit, I agree to the use of my personal information according to the Mercer Privacy Statement. I understand that my personal information may be transferred for processing outside my country of residence, where standards of data protection may be different.