Sites

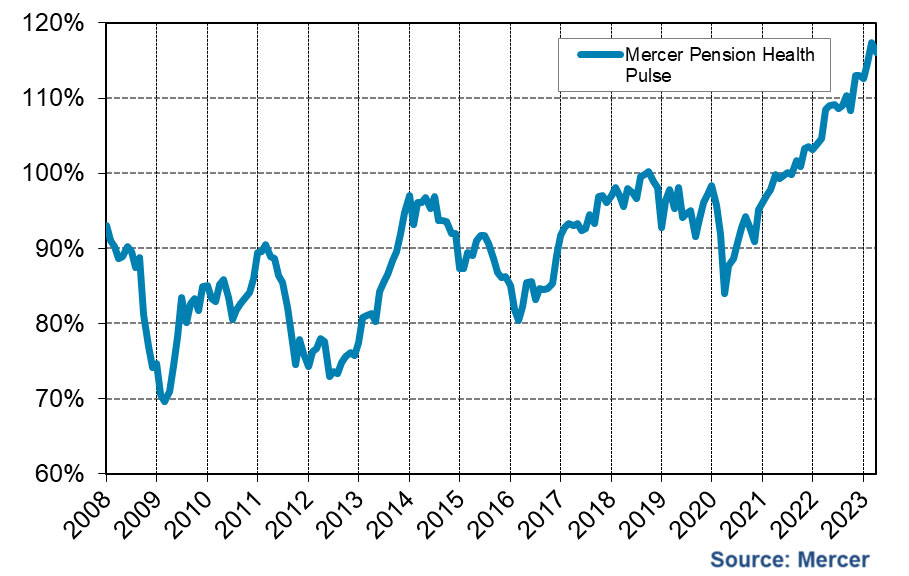

The Mercer Pension Health Pulse (MPHP), a measure that tracks the median solvency ratio of the defined benefit (DB) pension plans in Mercer’s pension database, rose during the first quarter of 2023, increasing from 113% at the beginning of 2023, to 116% at the end of the first quarter.

The first quarter saw improvements in January and February, with January’s improvement primarily driven by asset returns, while February’s improvement was primarily driven by increasing bond yields. However, these were partially reversed in March, as March saw a decline primarily due to decreasing bond yields, which can be attributed to the negative market sentiment caused by bank failures and concerns that these could lead to wider financial market contagion.

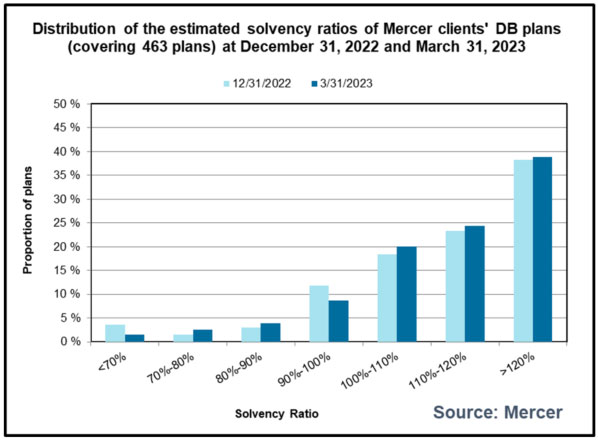

Of the plans in Mercer’s pension database, at the end of the first quarter, 83% are estimated to be in a surplus position on a solvency basis (vs. 79% at the end of Q4 2022). Approximately 9% are estimated to have solvency ratios between 90% and 100% (vs. 12% at the end of Q4 2022), 4% are estimated to have solvency ratios between 80% and 90% (unchanged from Q4 2022), and 4% are estimated to have solvency ratios less than 80% (vs. 5% at the end of Q4 2022).

“While markets continue to be affected by the volatility that was exacerbated by the banking crisis in the US and Europe, the financial health of most DB plans continues to improve” said Ben Ukonga, Principal and leader of Mercer’s Wealth business in Calgary. “With many plans being in better health than they have been in 20+ years”.

The global economy entered 2023 juggling multiple risks. Central banks globally were focused on bringing down inflation – by increasing their (respective) policy interest rates and engaging in quantitative tightening activities. On the heels of the failures of Silicon Valley Bank and Signature Bank, and the acquisition of Credit Suisse by UBS, the global banking system has come into focus. Policymakers must now weigh the consequences of continuing with monetary and quantitative tightening against the need to stabilize the banking sector, provide banks and other financial intermediaries with access to liquidity to keep global financial markets functioning, and not turn a banking crisis into a full-blown recession.

The war in Ukraine has resulted in significant loss of lives and has created a humanitarian crisis. The war also poses ongoing risk to the global economy, and there are no apparent signs of a resolution in the near term. The continuation of the war may lead to increasing global tensions, reduced trust and international cooperation, and a reduction in global trade – which will all negatively affect the global economy.

Closer to home, there is increased political polarization in the US. With the US debt ceiling needing to be raised, will Congress and the White House be able to compromise and come to an agreement to raise the debt ceiling? Or will both sides play to their respective bases and refuse to compromise. The consequences of a US Government debt default would be catastrophic to global financial markets.

In Canada, the Government of Canada’s decision to cease issuing real return bonds (RRBs) and to proceed with Bill C-228 raised eyebrows from pension stakeholders. In addition, with the recently released 2023 Federal Budget, will the spending plans outlined by the Government pour fuel on the inflationary fire, complicating the efforts of the Bank of Canada in bringing inflation under control?

RRBs are a key tool used by pension plans and insurance companies in hedging inflation and managing risk. Eliminating the issuance of new RRBs will (eventually) eliminate this key hedging tool. Although alternative assets are available to manage inflation risk, they are less direct at hedging against Canadian inflation, and add additional risk, complexity and cost with their use. Worthy of note, if the Government of Canada maintains this decision, Canada will be the only G7 country that does not offer inflation-linked bonds, and the decision was made in a period of high actual inflation.

Bill C-228 is a bill designed to provide pension deficits with super priority ahead of secured and unsecured creditors in the case of a plan sponsor bankruptcy or arrangement with creditors. The passage of the bill could have unintended consequences for DB plans, their sponsors and ultimately DB plan members. DB plan sponsors will likely face higher borrowing costs and stricter loan covenants, as creditors demand higher compensation and additional protection for the increase in risk due to Bill C-228. DB plan sponsors that fall into financial distress may be unable to raise funds, and enter into bankruptcy proceedings, whereas in the absence of Bill C-228 there may have been a willing lender. The bill could also lead to some plan sponsors closing their DB plans, which would be contrary to the protection feature the legislation suggests.

As 2023 continues, DB plan sponsors will need to be prepared for continued financial market volatility, along with the resulting effect on the financial positions of their plans. Many plans will not be facing deficit contribution requirements, due to the improvements in financial positions in 2022, and many plans are in surplus positions. However, to maintain these surplus positions, and not reverse back into deficits, plan sponsors will need to ensure they have the appropriate investment and risk management strategies in place, along with robust governance programs.

“As any market observer knows, markets can be, and many times are, volatile. And in order to be able to navigate the volatility, appropriate risk management programs need to be in place,” said Ukonga.

From an investment standpoint

A typical balanced fund portfolio would have posted a return of positive 4.6% over the first quarter of 2023. Investor sentiment shifted numerous times over the period driven by central bank rhetoric and news about weakening global economy, strong employment figures, several banking failures and bailouts. Equity markets finished the quarter in positive territory driven by strong gains reported in January.

In North America, equities rallied into January given indicators that inflation had declined for the sixth month in a row, giving investors hope that the end of tightening monetary cycle was near. By end of January, stronger than expected employment figures and higher than expected producer inflation numbers changed the narrative causing a valuation contraction. In March, market movements shifted rapidly with changing narrative about a series of banking failures and subsequent bailouts, concerns about contagion and the health of the broader financial system, as well as the pressure for central banks to tackle inflation while balancing potential future banking failures. The banking sector was not spared in Europe with the deterioration of Credit Suisse and the subsequent takeover by UBS. Bond yields declined over the quarter across most major regions as investors priced in expectations of reduced bank lending which would be supportive for falling inflation and prospects for a less-hawkish Federal Reserve. Emerging markets underperformed developed equities over the quarter. Commodities performed poorly throughout the quarter with oil prices declining materially, despite Russia’s announcement of cut in production. REITs posted large gains at the start of the year, followed by declines in February as rates continued to affect both financing and property valuations before recovering in March. From a style perspective, growth was in favor as falling yields were supportive of valuations with higher future earning expectations.

Canada underperformed during the quarter relative to its global peers, driven primarily by declines in the energy sector. Despite the strength of the Canadian banking system, negative investor sentiment toward banks globally also hurt performance of the domestic financial sector in March. In real estate, the number of transactions were subdued relative to recent periods. Industrial transaction activity slowed but remained robust, while multifamily sales dropped below trend. Investor demand for traditional office and retail were muted. The Canadian dollar appreciated against US dollar in the last week of March and ended the quarter with a slight gain.

Canadian bond prices continue to swing driven by shifting investor sentiment towards the path of interest rates. Yields declined in January, increased in February and fell again in March, ending the quarter at lower levels. Long-term bonds outperformed both universe and corporate bonds during the period. In addition, mid-term rates remained below both short-term and long-term rates throughout the quarter.

“We are entering a stage when traditional lenders will be reviewing their balance sheets and may reduce their lending activity. These types of dislocations are typically supportive of private lenders. Investors should be proactive in evaluating opportunities created by these events while also focusing on finding a strong General Partner (GP) to pursue them with.” said Venelina Arduini, Principal at Mercer Canada. “Private market investors should expect increased capital call activity across all asset classes and review their fund sourcing and governance processes to meet such calls. Cybersecurity risks have also increased and investors should confirm any wire instruction changes directly with their GP.”

The Bank of Canada increased rates by 25 basis points in January while announcing in March that they would hold the key interest rate. The U.S. Federal Reserve however, increased their target rate twice over the quarter, with increments of 25 basis points in both January and March. Both Federal Reserve and Bank of Canada have reaffirmed its commitment to controlling inflation. They did not explicitly refer to any future increases but they instead noted that additional policy firming might be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return to target inflation amid resilience in job growth, pay increases and consumer spending.

The Mercer Pension Health Pulse tracks the median ratio of solvency assets to solvency liabilities of the pension plans in the Mercer pension database, a database of the financial, demographic and other information of the pension plans of Mercer clients in Canada. The database contains information on almost 500 pension plans across Canada, in every industry, including public, private and not-for-profit sectors. The information for each pension plan in the database is updated every time a new actuarial funding valuation is performed for the plan.

The financial position of each plan is projected from its most recent valuation date, reflecting the estimated accrual of benefits by active members, estimated payments of benefits to pensioners and beneficiaries, an allowance for interest, an estimate of the impact of interest rate changes, estimates of employer and employee contributions (where applicable), and expected investment returns based on the individual plan’s target investment mix, where the target mix for each plan is assumed to be unchanged during the projection period. The investment returns used in the projections are based on index returns of the asset classes specified as (or closely matching) the target asset classes of the individual plans.

About Mercer

Mercer believes in building brighter futures by redefining the world of work, reshaping retirement and investment outcomes, and unlocking real health and well-being. Mercer’s approximately 25,000 employees are based in 43 countries and the firm operates in 130 countries. Mercer is a business of Marsh McLennan (NYSE: MMC), the world’s leading professional services firm in the areas of risk, strategy and people, with 85,000 colleagues and annual revenue of over $20 billion USD. Through its market-leading businesses including Marsh, Guy Carpenter and Oliver Wyman, Marsh McLennan helps clients navigate an increasingly dynamic and complex environment. For more information, visit http://www.mercer.ca. Follow Mercer on Twitter @MercerCanada.